---------------------------------------

By Jeff Goldsmith

Years ago, the largest living thing in the world was thought to be the blue whale. Then someone discovered that the largest living thing in the world was actually the 106 acre, 47 thousand tree Pando aspen grove in central Utah, which genetic testing revealed to be a single organism. With its enormous network of underground roots and symbiotic relationship with a vast ecosystem of fungi, that aspen grove is a great metaphor for UnitedHealth Group. United, whose revenues amount to more than 8% of the US health system, is the largest healthcare enterprise in the world. The root system of UHG is a vast and poorly understood subsidiary called Optum.

At $226 billion annual revenues, Optum is the largest healthcare business in the US that no-one knows anything about. Optum by itself has revenues that are a little less than 5% of total US healthcare spending. An ill-starred Optum subsidiary, Change Healthcare, which suffered a catastrophic $100 billion cyberattack on February 21, 2024 that put most of the US health system on life support, put its parent company Optum in the headlines.

But Change Healthcare is a tiny (less than 2%) piece of this vast new (less than twenty years old) healthcare enterprise. If it were freestanding, Optum would be the 12th largest company in the US: identical in size to Costco and slightly larger than Microsoft. Optum’s topline revenues are almost four times larger than HCA, the nation’s largest hospital company, one third larger than the entirety of Elevance, United’s most significant health plan competitor, and more than double the size of Kaiser Permanente.

If there really were economies of scale in healthcare, they would mean that care was of demonstrably better value provided by vast enterprises like Optum/United than in more fragmented, smaller, or less integrated alternatives. It is not clear that it is. If value does not reach patients and physicians in ways that matter to them—in better, less expensive, and more responsive care, in improved health or in a less hassled and more fulfilling practice—ultimately the care system as well as United will suffer.

What is Optum?

Optum is a diversified health services, financing and business intelligence subsidiary of aptly named UnitedHealth Group. It provides health services, purchases drugs on behalf of United’s health plan, and provides consulting, logistical support (e.g. claims management and IT enablement) and business intelligence services to United’s health plan business, as well as to United’s competitors.

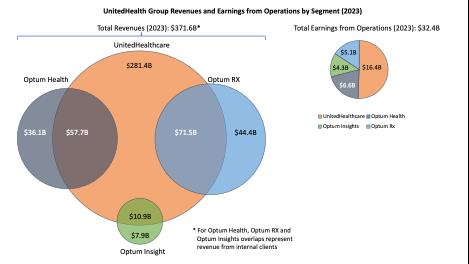

Of Optum’s $226 billion topline, $136.4 billion (or 60% of its total revenues) represent clinical and business services provided to United’s Health Insurance business. Corporate UnitedHealth Group, Optum included, generated $29 billion in cashflow in 23, and $118.3 billion since 2019. United channeled almost $52 billion of that cash into buying health-related businesses, nearly all of which end up housed inside Optum.

Source: 2023 UNH 10K

For most of the past decade, Optum has been driving force of incremental profit growth for United. Optum’s operating profits grew from $6.7 billion in 2017 (34% of UHG total) to $15.9 billion in 2023 (55% of total). However, the two most profitable pieces of Optum by operating margin—Optum Health and Optum Insight—have seen their operating margins fall by one third in just four years. The slowing of Optum’s profitability is a huge challenge for United.

Gaul Had Three Parts, So Does Optum

The largest and least profitable (by percent margin) piece of Optum is its giant Pharmacy Benefit Manager, Optum Rx, the third largest PBM in the US.

Optum Rx is more than half of Optum by revenue ($116.1 billion) but less than a third of its profits. The core of its profit comes from rebates from drug companies for featuring their drugs on OptumRx’s formulary- which governs which drugs United Healthcare subscribers get access to and how much they pay for them. Optum Rx derives almost 62% of its revenues from managing pharmaceutical spending for United’s health plan, but the remainder for servicing both health plan competitors of United and self-funded employers. It is the most “vertical” piece of Optum—in that it has the highest share of its revenues coming from United out of all of Optum’s major segments.

The accounting for these rebates is, to put it gently, less than transparent. Some of these rebates are returned to UHG customers (such as self-funded employers). Some are returned to insurers other than United for which Optum Rx processes pharmaceutical claims. And some are kept as profit inside either Optum Rx or United’s health insurance business. Optum Rx does not disclose the ultimate destination of many billions in rebates.

This lack of transparency is, understandably, a subject of political controversy. Congress is considering tightening PBM disclosures and possibly redirecting the flow of rebates back to health-plan customers and, gasp, potentially to patients themselves. Given the widening political controversy about whether PBMs actually save consumers money, Optum Rx’s business model is a major strategic vulnerability for UHG.

The second major piece of Optum, OptumInsight, has been in the glare of public controversy since its Change Healthcare subsidiary was hacked by the mysterious Russian hacker collective BlackCat in February. Its main business lines are: business intelligence, consulting, IT enablement, and business process outsourcing to non-UHG health enterprises. OptumInsight is the smallest of Optum’s three pieces at $18.9 billion, but the most profitable—22.5% profit margin—$4.3 billion in operating earnings. I have written extensively about OptumInsight, almost 42% of whose revenues derive from servicing United’s other businesses, but will not repeat that analysis here.

Optum Health

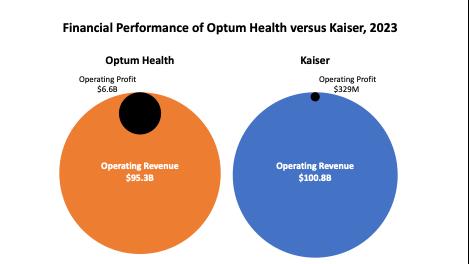

The piece we want to focus on here is the largest generator of profits for Optum, Optum Health, a diversified healthcare services enterprise. Optum Health is a $95.3 billion business, which makes it the second largest care enterprise in the US after Kaiser Permanente. It generates nearly $6.6 billion in operating profit for United. However, Optum Health’s profit margin declined from more than 10% in 2018 to about 6.6% in the third quarter of 2023. If not turned around, Optum Health’s declining profitability is a threat to United’s enterprise valuation and reputation. This is why when Optum reported disappointing 3Q23 earnings, United’s Chairman Steven Hemsley cleaned house at Optum Health, installing new leadership.

Since United is not required to disclose acquisitions that are not “material”, there is no way of knowing what United has actually bought and what it presently owns. But Optum Health is home to an enormous collection of physician groups, surgicenters, a large urgent care network, and two of the largest home health agencies in the US. It is a sprawling nationwide roll-up of healthcare assets.

Optum claims 90 thousand physicians in its networks but is cagey on how many are actually employed by Optum and how many are independent physicians in Independent Practice Associations that wrap around the employed groups and are common in the West and Southwest. An educated guess would be that Optum employs from 45 to 60 thousand physicians. If true, this would still be between double and triple the size of Permanente Medical Groups. Optum’s profitability dwarfs that of Kaiser (see below), perhaps a function of Kaiser operating 39 hospitals and Optum not operating a single one.

Source: UNH 10K, Kaiser Annual Report

Optum Health receives $57.7 billion (or 60% of its total revenues) from United’s health plan—the vertical part. But it also claims $21.8 billion in premium income, e.g. capitation, from “non-affiliated” customers, namely health plan competitors of United’s health plans. That capitation represents almost 23% of Optum Health’s total revenues. In addition, Optum Health reports $14.1 billion in services income, almost certainly “fee-for-service” based income from other health plans. What share of Optum Health’s $6.6 billion in profits come from these contracts with United’s competitors is a compelling mystery, since this is not reported in United’s financial disclosures.

Whatever the profit split, Optum Health is very much dependent not merely on the kindness of strangers, but of competitors of United’s core business. An important and unknowable question is whether Optum’s contract renewals with those competitors have enabled it to recover the soaring costs of nursing coverage, temporary physician coverage, turnover and retirements, and other labor factors that have exploded in the wake of the COVID pandemic. Every care delivery enterprise in the US has faced rising people costs, as the largest care delivery enterprise in the US, these forces have not spared Optum.

Optum’s medical group acquisition strategy to date has targeted independent (e.g. non-hospital) medical groups with significant at-risk (e.g. “capitated”) populations, mainly in Medicare Advantage plans. These included the original asset, the Nevada based Sierra Medical Group which United acquired when it purchased the Sierra Health Plan in 2007, but also Healthcare Partners, Monarch and North American Medical Management (based in Los Angeles), WellMed in central Texas, Atrius and Reliant in Massachusetts, Everett and PolyClinic in Seattle and Kelsey Seybold Clinic in Houston Texas. It is a growing presence in Oregon, New York and Connecticut through mainly smaller acquisitions. The map below showed where Optum Health’s assets were as of 2022.

The Vertical Integration Conundrum

Healthcare strategists have touted the idea of vertical integration –pioneered by Kaiser Permanente—which offers a comprehensive healthcare service experience—pretty much soup to nuts—through its health plan. The only way to access Kaiser physicians and hospitals is by enrolling in their health plan. Vertical integration has been viewed as a way of reducing health cost (by eliminating middlemen’s profits) and procuring products and services more efficiently, though actual evidence that it does so is scarce upon the ground.

With United, the health plan preceded the health services. In the first thirty years of its existence, United was a “network” plan, which contracted with independent hospitals and doctors for care. With the Sierra acquisition in 2007, United embarked on an adventure in strategic ambiguity—owning physician clinics which provided care to United customers as well as those of competing health plans. After Sierra and WellMed, a large capitated medical group in central Texas that Optum acquired in 2011, Optum’s medical group acquisitions have been, at best, loosely tied to United’s health plan enrollment. A 2018 analysis showed at best modest overlap between United’s Medicare Advantage market presence and the Optum Health network.

Making United “more vertical” in Optum markets would be complicated. Offering financial incentives to the Optum Health patients presently enrolled in competing plans to switch to United would pose two challenges. One is that this would damage Optum Health’s contracts with competing health plans. And sharing savings (e.g. some of United’s profits) with patients to redirect their care or lowering their rates would reduce health plan profit margins.

Conversely, telling Optum patients that they could only get care if they enrolled in United’s health plan would trigger a firestorm of negative publicity not to mention retaliation and cancelled contracts by United’s health plan competitors. Telling United subscribers they could only get care from Optum physicians and facilities would overwhelm them in volume and trigger longer waiting times and provider burnout. In sum, it does not appear to make business sense for United to make Optum more “vertically aligned” with its health plans. So straddling competitors in local markets seems to be an ambiguity with which United will have to cope going forward.

How much unregulated and invisible profit United’s health plans can generate “inside” United’s visible and highly regulated medical loss ratio (MLR) by selectively and generously compensating Optum’s physicians, surgical facilities, etc. is the most compelling mystery of this business model. Matthew Holt, a veteran industry observer, has termed this strategy of maximizing enterprise profit through contracting favorably with yourself “provider fracking.” Companies that control both insurance and care delivery have a great deal of flexibility in what the accountants term “transfer pricing”. This flexibility is valuable and would be lost were Optum to be spun off in a future United restructuring.

Two Big Risks for the Partially Integrated Optum Health

There are two other major clouds on the horizon for Optum Health. One is the Federal Trade Commission’s proposal to ban of non-compete clauses for corporate employees, including physicians. Non-compete clauses effectively make the patient populations of acquired physician groups the property of Optum. If physicians leave Optum, they are required to move out of the community to practice, surrendering their patients to the company.

Many of the senior physicians who were equity holders in the large practices acquired by Optum departed millionaires with United’s cash, leaving behind junior colleagues to suffer through both Optum system conversions and leadership changes that affected their daily lives as practitioners. Outlawing non-competes would enable disgruntled Optum physicians to remain in their home communities and take their patients with them.

If FTC precedents hold, the non-compete clause prohibition might not apply to non-profit hospitals (80% of all hospitals are non-profit), putting Optum and other corporate employers of physicians at a competitive disadvantage. In my opinion, entities that rely on coercive measures like non-competes to assure physician loyalty need to take a long hard look at their corporate culture.

The FTC’s proposed ban on non-competes is a major enterprise risk for Optum Health’s vast agglomeration of medical groups. If enacted, it would force Optum management directly to address physician working conditions, values, and priorities. United does have the potential for markedly reducing the documentation burden for Optum physicians that take care of United patients by selectively altering its claims review strategies. It will be interesting to see if they do so.

E Pluribus Unum

The other major cloud on the horizon is the unionization of physicians. According to AMA, some 67 thousand practicing physicians (e.g. not interns, residents or fellowship trainees) are members of labor unions. There are been several recent high profile instances where disillusioned hospital-employed physicians elected union representation (Allina in Minneapolis/St Paul, Providence St. Vincent and Legacy Health in Portland OR, are recent examples).

Unionization is often not motivated directly by compensation issues but rather by a sense of powerlessness and a feeling that core issues that affect the employee are not being addressed. Unionization would both increase Optum’s operating costs and reduce its management’s flexibility. Optum Health’s groups are by far the largest and most lucrative target of physician unionization in the United States.

Down in the Valley

The emerging market risks for Optum can be seen in two medium sized cities in Oregon’s Willamette Valley. During the early pandemic, Eugene-based Oregon Clinic encountered terminal operating difficulties and sold to Optum in late 2020. In March of this year, Optum sent letters to patients of departing Oregon Clinic physicians that they would have to find care elsewhere because they were unable to recruit replacements for their physicians. These 32 physicians resigned, apparently, because they were unhappy with working conditions at Oregon Clinic after the Optum takeover. Reading between the lines, due to non-competes, the departing physicians were unable to remain the Eugene area and thus unable to continue seeing long-standing patients.

Meanwhile, up the road forty miles in Corvallis, Optum requested that the State of Oregon expedite review of its proposed acquisition of the Corvallis Clinic due to accelerating cash flow difficulties that made it impossible for the Clinic to meet its payroll. The State ultimately acceded to Optum’s request. The apparent cause of the cash flow problem: the Change Healthcare cyberattack, which made it impossible for Change, an Optum subsidiary to accept or pay claims from its provider networks, including, most likely Corvallis Clinic. In other words, the catastrophic system failure of one piece of Optum likely accelerated another piece of Optum’s acquisition of the largest physician group in town.

Taken together, these simultaneous problems have not served to enhance Optum’s image as a care provider in the southern Willamette Valley. They make the company appear as a cold and exploitative outsider capitalizing on problems it helped create. These events will not enhance the likelihood of United growing its core insurance business in the area or endear the company to Oregon’s health system regulators, or its state managed Medicaid program, the Oregon Health Plan.

Outgrowing Its Nervous System?

Optum Health has almost quadrupled in size in the past six years, but its profit margin has fallen by a third. Given the explosive pace of acquisitions and the cost pressures on physician practices during and after the COVID pandemic, this margin deterioration is not surprising. However, if Optum Health’s new management does not stabilize its operating performance, margins could deteriorate further, putting pressure on United’s earnings.

There are no evident economies of scale or co-ordination in physician services. How Optum can recruit and retain high quality motivated physicians and advanced practice nurses to its vast care system is a major challenge to the enterprise. They will need a compelling answer to the question: “Why work for Optum?” The answer cannot be: we are huge and you don’t have a choice. How the company creates value for its tens of thousands of physicians and nurses will be the central management facing United, or indeed any large-scale employer of these complex professionals.

There is growing evidence that there are diseconomies both of scale and co-ordination in health services generally. Those diseconomies manifest themselves in the vast empty space between the giant enterprise and the physicians and patients who rely on them. Every denial of care by United’s AI-driven claims management system makes a tiny dent in the company’s consumer image. Patient anger over arbitrary and self-interested health plan meddling in care decisions resulted in first managed care backlash in the late 1990’s. United’s recent Net Promoter Score of -5 suggests that it has a long way to travel to regain customer confidence and loyalty.

The physician-patient relationship remains the bedrock of the health system. If the nerve endings of an enterprise do not reach out and sense the effect it is having on that relationship, it isn’t going to be very long before it either ceases to grow or ceases to be profitable or, likely, both. United and Optum have reached that tipping point right now. Follow Optum’s physicians and their patients and see the future.

Acknowledgements: Trevor Goldsmith provided research and technical support for this piece. The author appreciates Ian Morrison, Andrew Mueller and Jamie Robinson for reading and commenting on this piece.

Jeff Goldsmith is a veteran health care futurist, President of Health Futures Inc and regular THCB Contributor. This comes from his personal substack

-----------------------------------------

By: matthew holt

Title: Optum: Testing Time for an Invisible Empire

Sourced From: thehealthcareblog.com/blog/2024/04/02/optum-testing-time-for-an-invisible-empire/

Published Date: Tue, 02 Apr 2024 08:43:00 +0000

Read More

Did you miss our previous article...

https://prohealthsciences.com/general-health-and-wellness/the-perks-to-being-a-sociopath