---------------------------------------

By TREVOR VAN MIERLO

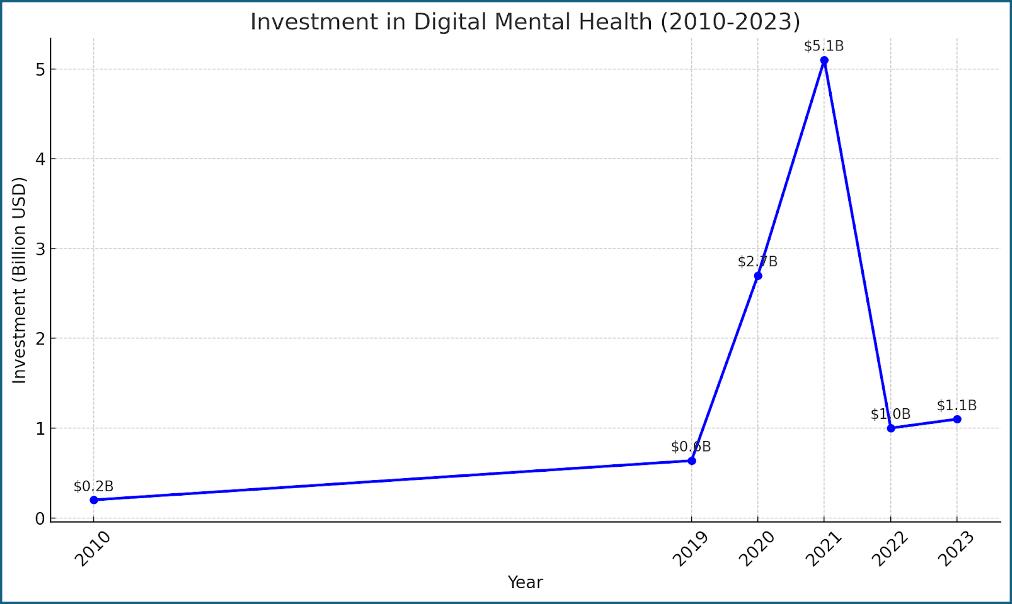

In 2021, digital mental health and substance use startups attracted a record-breaking $5.1 billion in funding. Despite the surge, the promise of scalable, transformative digital health platforms remains unfulfilled.

Following the surge, investment plummeted. Unlike other industries that have been revolutionized by digital-first solutions, digital health struggles with models that fail to address cost, complexity, and access.

What we’re left with entering into 2025 are a smorgasbord of solutions clamoring to attach themselves to traditional enterprise incumbents (Health Insurance Providers, Electronic Health Records, Hospital Systems). These incumbents have achieved scale – but not the type of scale that digital health needs to flourish.

Digital Mental Health Investment (2010-2023)

Incumbents Build Deep, Startups Go Wide

Incumbent scale is infrastructure-heavy, slow, and linear, and focuses on deep integration within their established markets.

In contrast, startups aim for technology-driven, exponential, and global scale, leveraging digital platforms to serve millions of users quickly. While startups have the speed advantage, achieving scale similar to incumbents requires win-win partnerships and fundamental shifts away from established business models.

Incumbent Scale vs. Startup Scale

Incumbent Scale vs. Startup Scale

The investment market does see the tremendous opportunity: a massive, growing global customer-base proactively demanding help as social stigma decreases. And as time passes, this customer-base grows exponentially with technology pervasiveness.

What investors see is unmet demand for mental health and substance use treatment, and a historic opportunity for digital health to step up and deliver solutions that are scalable, accessible, and affordable.

However, the delivery mechanism to these populations, though digital, is obfuscated through the blurred lens of incumbent purchasing power. We can’t get past incumbents’ size, their reach, and their connection to patients. In this common view, incumbents are the customer. This view is promoted by both industry and academia.

A recent HLTH Inc. summary, titled Boston Think Tank: Event Takeaways – Scaling Digital Health: De-Risking Adoption summarizes this: “To effectively scale digital health solutions, a carefully crafted strategy is needed – one that meets the intricate demands of healthcare systems while navigating potential adoption hurdles“.

Last April a JMIR Publications published Digital Health at Enterprise Scale: Evaluation Framework for Selecting Patient-Facing Software in a Digital-First Health System. It begins: “The digital transformation of our health care system will require not only digitization of existing tools but also a redesign of our care delivery system and collaboration with digital partners.“

Both will take decades to achieve, and the market won’t wait. The customer is not the incumbent. The customer is not even patients – it’s people.

For now, demand surges, but digital health is stuck in the middle.

Demand Surge: Mental Health & Substance Use TAM, SAM, and SOM

To understand the scale of the opportunity in digital mental health and addictions, we turn to TAM (Total Addressable Market), SAM (Service Available Market), and SOM (Serviceable Obtainable Market) – frameworks widely used by investors to evaluate market potential. The framework is summarized nicely by Ali Gamaleldin here.

The TAM, SAM, and SOM in mental health and addictions represents an extraordinary, if not immense, business opportunity far surpassing many other industries in scope. The size of the market is a result of high prevalence (1 in 8 citizens), persistent demand, and global scalability after the proper solution is implemented.

In North America and Europe alone, the annual TAM for mental health and substance use assistance is currently estimated at $1.2 trillion.

TAM, SAM, and SOM for North America and Europe: Mental Health and Substance Use

TAM, SAM, and SOM for North America and Europe: Mental Health and Substance Use

In Australasia the TAM, SAM, and SOM are estimated at $60, $15, and $3 billion, respectively. A lack of comprehensive epidemiological data prohibits the TAM, SAM, and SOM from being calculated for Asia, but growth opportunities are enormous. This is similar to Central and South America, which are further compounded by diverse economies and cultures, government-led healthcare systems, and cultural perceptions of mental health.

But despite setbacks in Asia, Central, and South America, the diverse, multicultural societies in North America and Europe can actively test and validate these emerging markets. Those regions are ripe for follow-on expansion and digital scale.

But has this been done before? What other industries have addressed opportunities with high TAM, SAM, and SOM? Is there a roadmap?

The Current Market and Roadmaps

Rock Health Capital appeared optimistic about 2024. However, in reality digital mental health companies only raised $682 million in the first half. MedTech Strategist reflect this cautious optimism, and Galen Growth | Insights You Can Trust states that digital health is poised to outperform 2023, but with the investment focusing on AI are these numbers indicative of digital health breakthroughs?

There are several factors behind the rapid decrease in funding from 2021, including a correction due to pandemic-driven surge, overvaluations, and investor fatigue, but markets are opportunistic.

But let’s face it – the primary reason is that despite the ongoing hype surrounding digital health, a clear winner – or winners – have not emerged. Worse – unlike other industries that have transformed to digital, we still haven’t seen a profitable business model.

Looking to Other Industries

In other industries, significant TAM, SAM, and SOM opportunities were leveraged to disrupt industry incumbents.

Successfully Scaling TAM, SAM, and SOM

Successfully Scaling TAM, SAM, and SOM

In the above examples, each company disrupted incumbents by addressing problems like cost, complexity, or access. Those of us in the digital health industry need to honestly ask ourselves if any of the solutions we’ve created have:

- reduced costs (one could argue healthcare is more expensive than ever)

- made the help seeking process and access less complex (try to obtain immediate access to a digital health product)

- opened doors to non-traditional customers (e.g. non-insured, minimally-insured, students, etc.)

Substitutions & Supplements

Digital health today is dominated by substitutes, like telehealth and digital therapeutics (mimicking traditional care), and supplements (engagement apps and wearables). These tools enhance failing models and do not address the TAM.

Disruptions vs. Supplements vs. Substitutions

Disruptions vs. Supplements vs. Substitutions

Neither approach addresses the core challenges of cost, complexity, and access. True disruption is still missing.

Digital Health: A Problem in Search of an Answer

Vast portions of digital health’s TAM remain untapped, and the problem is clear: while the demand for mental health and substance use interventions is enormous, traditional and hybrid models – focusing on dissemination through incumbents – fall short with high costs, and limited scalability.

What’s clear is that the rapidly expanding market, which is burgeoning globally, is ripe for disruption.

Catching the breath of digital health CEOs, product managers, and investors is that In the realm of digital health, a “winner-take-all” scenario is entirely possible. This means that a single evidence-based company or platform could potentially dominate the market by capturing a large majority of users and market share, generating global network effects, leveraging data – and perhaps most importantly – taking advantage of investor fatigue in ventures that are stagnant.

Digital health is at a crossroads. To truly revolutionize care, we must move beyond incremental improvements and embrace solutions that disrupt the status quo – solutions that scale globally, reduce costs, and open doors for the millions waiting to jump at accessible care.

Dr. Trevor van Mierlo has built mental health and patient support products for more than two decades and is the CEO of Evolution Health

-----------------------------------------

By: matthew holt

Title: Mental Health’s Unfinished Digital Revolution

Sourced From: thehealthcareblog.com/blog/2024/12/11/mental-healths-unfinished-digital-revolution/

Published Date: Wed, 11 Dec 2024 06:46:00 +0000

Read More

Did you miss our previous article...

https://prohealthsciences.com/general-health-and-wellness/what-it-really-means-to-get-an-abortion-after-fetal-viability