---------------------------------------

By SETH JOSEPH

This is part 3 of Seth’s series about Epic that has generated much interest and a little controversy and we are happy to host it on THCB. Part 1 and Part 2 were published on Forbes earlier this year.

According to people in the room, Judy Faulkner’s vision on stage at Epic’s 2022 User Group Meeting was epic, in the grandest sense of the word.

The company, which had grown as a unified clinical and billing EHR system, was now laying out a roadmap in which it would be the digital front door for all things consumer facing. A massive panoply of capabilities including, according to Epic’s own subsequent documentation, customer relationship management, provider finders and online scheduling, online check-in, patient financial experience, and many others.

Core to enabling all of this was shifting how patients interact with MyChart, the patient-facing application that allows individuals to access their health records.

Historically, each MyChart account was ‘tethered’ between an individual and a hospital system and represented a simple portal for the individual to view her records. If an individual had been seen at multiple different hospital systems, then she would have multiple separate MyChart “instances”, or entirely separate accounts and logins.

Now, Epic would ‘stitch together’ the health records and data from different hospitals on behalf of the individual in advancing what colloquially has been called Epic’s ‘national MyChart strategy’, and enable robust new functionality, creating compelling network effects between consumers and hospitals.

There were only a few problems with Epic’s strategy: first, many customers weren’t asking Epic to develop these capabilities; second, there were startups and incumbents already providing many of these capabilities; and third, the company was in a race with a federal agency, which was pushing for open standards and access that threatened Epic’s plans.

But for a company that had slowly and steadily become the dominant health technology player, whose staff meetings for a period ended half-jokingly on a slide with the words “World Domination” on them, these problems were all fixable.

The Promise Of Consumer Empowerment Tools

As modern history has demonstrated time and again, the ability to own or control the consumer entry point for technology can be a strategic advantage. Apple’s sleek product designs, user experience and tight ecosystem enable it to extract 30% of app developer revenues seeking to reach Apple’s users. Google’s dominance in search has positioned it to be the entryway to the internet for billions of consumers regardless of their ultimate destination, resulting in extraordinary revenue growth and profitability.

In healthcare, the ability to meaningfully engage consumers through technology has long held promise of solving intractable problems, while also potentially positioning the firm that figures out how to do so as a new locus of power, similarly as Apple and Google above. Triaging care options for consumers, navigating them to lower cost services, facilitating payments, and providing modern convenience options are just a few of the hundreds of use cases that consumer-facing technology holds.

Key questions facing the firms seeking to find healthcare’s holy grail are how best to do this and where to start, as consumer habits and sentiment toward healthcare has proven challenging for tech companies to figure out.

For instance, tech giants Microsoft and Google had both placed significant bets on ushering a new era of consumer empowerment in the late-2000s, with Microsoft HealthVault and Google Health. Known as patient health records (PHR), the two companies sought to enable consumers to access, aggregate, store and potentially share their health records.

In retrospect, Microsoft and Google’s efforts were perhaps a bit too early, as both initiatives were shut down in the early 2010s, before an ecosystem of health technology adoption, connectivity and capabilities that could have feasibly supported their vision. And before consumers had a compelling reason to change their own use of technology to engage in their healthcare.

By 2022, however, the ecosystem had arrived. After the EHR Incentive program, more than 90% of doctors and hospitals had EHRs. The Covid-19 pandemic drove rapid adoption of telehealth by both physicians and consumers. Approximately $100 billion in venture capital had flowed into health technology innovation. New price transparency policies were shedding sunlight into formerly opaque and labyrinthine contracting practices. The 21st Century Cures Act put teeth into driving interoperability, introducing information blocking as a civil penalty with million dollar fines. One industry group published a report titled “Unbundling Epic: How The EHR Market Is Being Disrupted.” This author proclaimed The EHR Is Dead.

If the EHR was dead or being disrupted, then every EHR company needed a survival plan.

Epic’s Fear And Unfair Advantage

According to one hospital executive, it was this backdrop that concerned Epic’s leadership: with a rapid influx of new players and a shifting balance of power, Epic might be relegated to “just being the pipes” while others capitalized on new opportunities. Given the company’s rigid belief – proven correct time and time again – that it alone would deliver the best results for its customers and consumers, Epic thought such an outcome would be a disaster.

To combat this risk, Epic by mid-2022 had a new strategy with MyChart and network effects at the heart of it.

Prior to this point, Epic had allowed its hospital customers to build their own consumer-facing applications on top of the MyChart chassis, or to bring in third-party solutions to sit on top of and integrate with MyChart. To support this, Epic provided software development kits (SDKs) to customers, and allowed integration options to third party vendors.

Supporting this innovation was important to some Epic customers. In particular, larger health systems (typically those with more resources and sophistication) viewed their consumer-facing capabilities as an important way to differentiate themselves in the market.

The new strategy entailed driving adoption and utilization of MyChart (already the best known patient-facing application in the country), developing new consumer-facing capabilities and pushing hospitals to use those, and capturing consumers as their preferred application of choice.

In short, Epic sought to expand its sphere of influence, from a position of market dominance over one sector of healthcare (hospital systems) into another: consumers.

To do so, Epic crafted a coherent policy and set of tactics designed to persuade hospitals to get on board with its vision, muscle out competitors, and influence regulation in order to achieve its ends.

Epic’s Tactics Leverage Its Strengths, But Raise Important Anti Competitive Questions

As previously reported, Epic arguably has a monopoly position with its inpatient EHR among multi-hospital health systems and academic medical centers. Since that reporting, Epic has continued to gain market share; its software is now used at hospitals accounting for 51% of all beds nationwide. As multiple hospital executives have put it in conversations, Epic is running away with the EHR market.

The EHR may be commonly thought of as a clinical application, but it may be more accurate to think of it as the hospital’s operating system. The distinction can be important: an application provides workflow capabilities to achieve a specific objective, while an operating system acts as an interface between the user and hardware that controls the rules by which applications function and the resources it has access to.

Consider that while doctors and clinicians use the EHR as an application, it looks different from the hospital enterprise perspective: the EHR is the default system that its most highly trained, paid and busiest staff interact with every day, rendering it the single most important system; the data entered by clinicians stores patient records and associated information that is used for mission-critical purposes including billing, reporting, and audit functions; and accordingly, it is the system which virtually every other application must accordingly integrate with (and not vice versa).

As the hospital’s ‘operating system’, Epic’s national MyChart strategy starts out with natural built-in advantages versus patient-facing technology competitors, including:

- MyChart footprint: The federal Meaningful Use Program required hospitals to use EHRs that provided a patient portal. Today, Epic’s MyChart boasts between 190M and 300M consumer accounts, an incredible early advantage given the increasing utilization of personal health records.

- Key consumer infrastructure and integration: A patient portal is of limited utility to a consumer. But one that starts out integrated with the provider system, allowing single-sign on, scheduling, messaging, telehealth and related ways the consumer may want to interact with her provider, can provide substantial value.

- Hospital relationships and trust: The value of being able to roll out new capabilities to existing customers representing 60% of all health system spend at a single event (in this case, the 2022 Epic user group meeting) cannot be overstated. Nor can the years and, oftentimes, decades of trusted relationships that Epic has cultivated with its customers.

According to hospital and industry executives, Epic is in the process of pulling all of these levers. And while some competitors may complain about these built-in advantages, the reality is that Epic is dominant in the inpatient EHR market for good reason, and it’s a smart strategy to leverage its existing strengths across product, capabilities and relationships to advance its national MyChart vision.

However, some of Epic’s other tactics, though they may prove to be incredibly effective, raise questions. Here are four in particular:

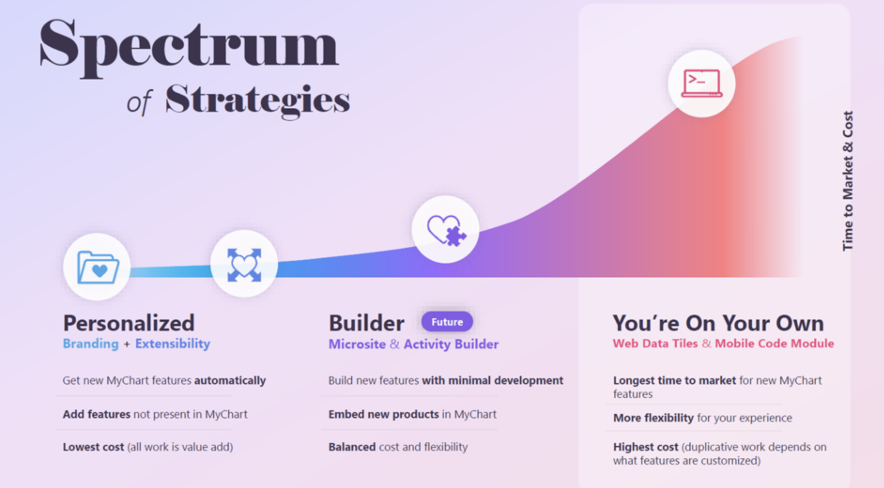

1. “You’re On Your Own”: A yoyo can mean a foolish or incompetent person, a term Epic has decided to apply to some of its customers. At the company’s 2022 user group meeting, Judy Faulkner introduced the term “you’re on your own” (yoyo) to refer to Epic hospital customers who wanted to maintain their own digital front-door strategy. Shifting from its historical stance of being agnostic as to whether hospitals used only Epic’s MyChart or preferred to develop their own consumer-facing strategy that integrated with MyChart, Epic made clear it wanted hospitals to forgo their own strategy and get on board with a more Epic-controlled version of MyChart. Consistent with this desire are Epic materials that clearly demonstrate feature divergence for customers adopting its preferred ‘Personalized’ version of MyChart versus feature discrimination for those ‘yoyo’ customers.

2. Changing Fee Structure For ‘Yoyos’ and Raising Prices To Steer to MyChart: According to executives from multiple systems who found themselves being called ‘yoyos’, Epic also subsequently and unilaterally has attempted to change its fee structure for technology and support costs related to MyChart. Historically, Epic charged a flat fee to support hospitals who either built their own consumer-facing applications that integrated with MyChart or partnered with commercial vendors for the same purpose. After it announced its national MyChart strategy, however, Epic began notifying ‘yoyo’ customers that it was shifting to a new pricing structure based on the number of consumers the hospital served. Several hospital executives mentioned that this would increase the relevant MyChart fees by several thousand percent, from tens of thousands of dollars annually to millions; the alternative was to avoid these incremental fees by abandoning their own consumer-facing strategies and opting in to Epic’s national MyChart strategy.

In response to questions about these changes, an Epic spokesperson noted that MyChart fees themselves had not changed since 1999. With respect to technology and support costs, the spokesperson noted, “With ‘You’re On Your Own,’ customers can choose to license additional tools that allow their developers to embed parts of MyChart into their own customer applications.”

3. Eliminating Preexisting Interoperability Access: Epic had historically supported its ‘yoyo’ customers, in part, by providing MyChart integration and interoperability resources to vendors that those customers choose to work with for consumer-facing applications. With the introduction of its national MyChart strategy, however, Epic has begun restricting access to those resources. In some cases, Epic has allegedly let slip to some vendors, including those they have worked with for years collaboratively, that they are now competitors, and that Epic would be “sunsetting” (eliminating) existing interoperability resources and that the vendors would not have access to future iterations of the same resources.

Based on a review of an Epic email response to an individual requesting the status of previously available resources, what Epic appears to be doing in some cases is withdrawing application programming interfaces (APIs) from its open.epic site, and shifting those to its ‘Vendor Services’ program. An initial challenge for any vendor seeking to integrate with Epic is that APIs in its Vendor Services program are not published or discoverable. A vendor seeking to apply to this program must first fill out and submit a questionnaire, but Epic provides no guidance on what the criteria for inclusion or exclusion are, nor how it determines what API resources will be available or to whom. This practice exposes Epic to claims that it may be picking winners and losers.

4. Delaying Standards (Which May Drive MyChart Adoption): The National Institute of Standards and Technology is a branch of the U.S. Department of Commerce. Its IAL2 standard is intended to allow for remote identity proofing, which is necessary to enabling a future in which individuals can request and access their own medical records from existing health information networks that providers use routinely. Enabling individuals to use digital applications of their choice to access their records is a priority for ASTP/ONC, the federal agency responsible for promoting interoperability. Epic announced in August that they would support this capability, but with a twist: the company supports the IAL2 standard to allow individuals to locate where they have received care, but not to request and retrieve their records.

Some industry cynics have privately claimed that Epic’s stance will result in individuals still needing to have an existing or create a new MyChart account, which may increase fees Epic charges to hospitals (as MyChart fees are volume-based) and increase lock-in of Epic’s ecosystem.

An Epic spokesperson flatly denies this, noting “Use of MyChart strictly for authorization to share data via OAuth 2.0 [another technical standard for identity authorization] does not increment any MyChart subscription counter, does not result in any additional charges to our customers, and is unlikely to attract new users to MyChart.”

————–

Individually, each tactic may support a legitimate business purpose. For instance, while “yoyo” might seem a crude term, it’s consistent with Epic’s generally playful and creative naming conventions. Changing its fee structure may reflect Epic making a course correction to a costly way of supporting customers, as an Epic spokesperson suggested. And as industry insider and analyst Brendan Keeler has noted, Epic is a leader among EHRs when it comes to enabling individual access services, so it’s hard to critique.

Taken altogether, however, the collective tactics are enough to have some industry insiders and investors concerned that they are anticompetitive.

Is Epic Unfairly Pressing its High Ground Advantage?

Having grown organically since 1979 and only in the past decade becoming the leader in EHR, it’s possible that Epic’s insular culture blinds it to its own market strength and influence in adjacent markets.

If so, it may behoove Epic to reflect on issues involving fellow tech giants who leveraged dominant market positions in one business to unfairly and illegally advantage themselves when facing technology shifts and changing consumer behavior. Most relevant may be the Microsoft lawsuit, in which Microsoft was found to be illegally utilizing its dominant position as an operating system to exclude competitors in the emerging web browser market. And the more recent case against Google, in which Judge Mehta found the company recognized the power of default placement and distribution to illegally secure and expand its position.

In Epic’s case, the company holds a dominant position as the hospital’s operating system. By removing existing APIs and interoperability resources to consumer-facing companies and changing fee structures, it is making it more cumbersome and expensive for hospitals to select alternative patient-facing technologies, making MyChart the default path forward. One outcome is the perception that its tactics are exclusionary in nature and foreclose on innovation in an emerging market. Another result, also problematic for Epic, is reduced consumer choice and increased direct costs (to hospitals) and indirect costs (to competitors and consumers).

Yet, Epic arguably does not need to employ these tactics to win. MyChart seems well-positioned to end up as the most robust, seamless and compelling ecosystem for consumers as a result of Epic’s trusted relationships with hospitals, dominant market share and existing (and growing) network effects.

For the time being and absent any force majeure preventing Epic from executing its plan, it looks like Epic’s consumer strategy is likely to result in network effects that even more firmly entrench the company’s position and establish another locus of power. If successful, Epic could find itself in a position like Apple, with the ability to extract a substantial revenue share from any developer seeking to access consumers for whom Epic would be the default “digital front door”.

If you work in Verona Wisconsin, this is a good thing. Maybe too, if you’re a consumer.

Seth Joseph is the Founder and Managing Director of Summit Health Advisors

-----------------------------------------

By: matthew holt

Title: Epic’s Consumer Strategy Is Bold. Its Tactics Push The Boundaries.

Sourced From: thehealthcareblog.com/blog/2024/11/19/epics-consumer-strategy-is-bold-its-tactics-push-the-boundaries/

Published Date: Tue, 19 Nov 2024 06:06:00 +0000

Read More

Did you miss our previous article...

https://prohealthsciences.com/general-health-and-wellness/how-to-get-through-the-holidays-while-on-a-weight-loss-drug